High Income vs Low cost of Living Paradox

Arjun K A

1/5/20268 min read

The Wealth Gap: Why PPP Matters When Comparing India to the World

If you’ve ever wondered why $100 feels like a fortune in a small town in India but barely covers a steak dinner in New York, you’ve stumbled upon the world of Purchasing Power Parity (PPP).

There is a common debate among young professionals and families today: Is it better to earn a decent salary in India with a low cost of living, or a high salary in a developed nation like the US or Australia where everything is expensive?

To answer that, we have to look past the raw numbers and understand the "Global Wealth Gap." While India is one of the fastest-growing economies in the world, its PPP per capita remains significantly lower than nations like the US, UK, Canada, and Singapore.

In this guide, we’ll break down what this means for your pocket, your lifestyle, and your future.

What Exactly is PPP? (The "Big Mac" Logic)

Before we compare countries, let’s simplify the jargon. Purchasing Power Parity (PPP) is an economic metric used to compare the standard of living between countries by eliminating differences in currency exchange rates and the cost of goods.

Imagine a basket of goods—bread, milk, internet, and a haircut.

In the US, that basket might cost $50.

In India, the exact same items might cost ₹1,500 (about $18).

Even though the exchange rate says $50 is worth more than ₹4,000, your ₹1,500 in India buys you the same "lifestyle" as $50 in America. PPP adjusts for this, allowing us to see how much "bang for your buck" you actually get.

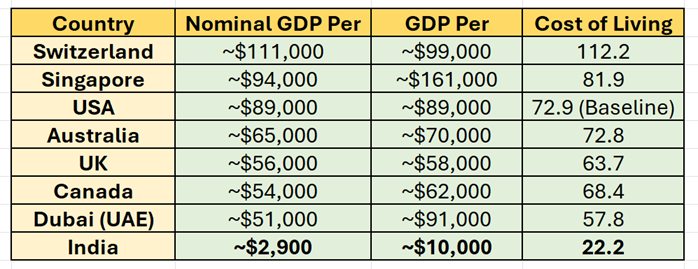

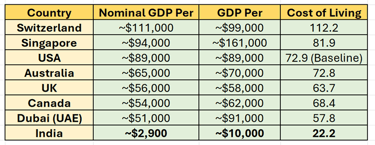

India vs. The Giants: The Numbers Game

When we look at PPP per capita (the average economic output per person, adjusted for local costs), the gap between India and developed nations becomes clear.

While India offers a "comfortable" life for the middle class due to low cost labour and local produce, the total wealth generated per person is still a fraction of what is produced in the UK or Australia.

The "Dual Reality" of Living in India

Living in India presents a unique paradox. Because the cost of living is low, a salary of ₹15 Lakhs per year can afford you a lifestyle—complete with domestic help, home delivery, and frequent dining—that would require a salary of $200,000 in San Francisco.

The Advantage of India:

Services are of low cost: Labor-intensive tasks (cleaning, repairs, cooking) are affordable.

Basic necessities: Food, healthcare (out of pocket), and public transport are significantly low cost than in the West.

The "King" Lifestyle: You can live like royalty on a fraction of a Western salary locally.

The Disadvantage:

Global Goods: An iPhone, a MacBook, or a Tesla costs the same (or more due to taxes) in Mumbai as it does in London.

Imported Inflation: When you want to travel abroad or buy international brands, your Indian Rupees lose their "PPP advantage."

The Global Wealth Reality: Comparing India’s PPP to Developed Nations (2025-2026)

When we talk about "wealth," we often look at the wrong numbers. You might hear that India is now the 4th largest economy in the world, having recently overtaken Japan. While that is a massive achievement for the nation, it doesn't always translate to the wealth of the individual.

To understand why a middle-class professional in Singapore or Switzerland feels "richer" than one in India—even if they both have similar job titles—we need to look at Purchasing Power Parity (PPP) and the latest economic data.

The Data Breakdown: India vs. The World

The following table shows the stark difference between Nominal GDP per capita (raw dollar value) and PPP per capita (adjusted for local costs). These figures represent the latest 2025-2026 projections and 2024 benchmarks.

While India’s cost of living is nearly 4 times lower than the other developed nations, its average citizen’s purchasing power is roughly 9 times lower.

Understanding the "Purchase Power" Gap

The quote, "Developed economies provide far higher incomes and purchasing power abroad," refers to the Absolute Savings Potential. Let’s look at why this matters for a modern professional.

1. The High-Cost, High-Reward Cycle

In a country like Switzerland or Singapore, you pay more for a coffee or a haircut. However, your salary is so high that after paying for these "expensive" local services, the surplus money left in your bank account is good.

In India: You might earn ₹1,00,000 and spend ₹60,000 on a comfortable life. You save ₹40,000 ($470).

In the UK: You might earn £4,000 and spend £3,000 on a comfortable life. You save £1,000 ($1,270) (~₹108077)

Even though the UK is "expensive," the person in the UK has saved 3x more in absolute terms. This "Global Wealth" can be used to buy things that cost the same everywhere, like an iPhone, a or an electric vehicle.

2. The Tech and Luxury Tax

Technology is the great equalizer of PPP. A high-end smartphone costs roughly $1,000 globally.

For an American earning $80,000, that phone is 1.2% of their annual income.

For an Indian earning ₹10,00,000 (~$12,000), that same phone is 8.3% of their annual income.

This is why people in developed nations seem to have the latest gadgets and cars—it’s not that they are "spending more," it's that those items represent a much smaller "slice" of their total income.

The Future: Is India Catching Up?

The gap is narrowing. India is currently the fastest-growing major economy, with a growth rate of roughly 6.5% to 7%. As the country moves toward becoming a $5 trillion economy (projected by 2027-28), the PPP per capita will rise.

As more global companies set up "Global Capability Centers" (GCCs) in cities like Bengaluru and Hyderabad, Indian salaries for top talent are beginning to match global standards. When an Indian professional earns a "Western" salary while paying "Indian" costs, they effectively become some of the wealthiest individuals globally in terms of discretionary spending.

Conclusion: Weighing Your Options

If you are choosing between staying in India or moving to a place like Dubai or Canada, don't just look at the Cost of Living. Look at your Savings Potential and Global Purchasing Power.

Stay in India if you value local services, family proximity, and a rapidly growing domestic market where your money goes further for daily life.

Move Abroad if you want to build global wealth, travel the world easily, and access superior public infrastructure that "private wealth" cannot buy in India.

Ultimately, India offers a high "lifestyle" value while the countries like US, UK, and Singapore offer the highest leverage on the global stage.

FAQ’s

Section 1: The Basics of Global Wealth

1. What is PPP and why should I care?

Purchasing Power Parity (PPP) adjusts for the cost of living. It tells you what your money actually buys locally. It’s the difference between having a high salary in London but living in a tiny flat, vs. a lower salary in Pune while owning a bungalow.

2. Is India really the 3rd largest economy?

Yes, in PPP terms, India ranks 3rd (after China and the US). However, in Nominal terms (actual dollars), it is the 4th largest. The gap exists because goods/services are significantly lesser in India.

3. Why is India’s PPP per capita so much lower than Singapore’s?

Singapore has a tiny population and massive financial output. India’s total wealth is split among 1.4 billion people, leading to a lower "per person" share—roughly $10,000 (PPP) vs. Singapore’s $160,000+.

4. Does a low PPP mean India is poor?

Not necessarily. It means the average individual has less "global buying power," but their "local lifestyle" can still be comfortable due to low costs for essential services.

5. What is the "Big Mac Index"?

It's a fun way to explain PPP. If a burger costs $6 in the US but only ₹200 ($2.40) in India, the Rupee is "undervalued" by PPP standards.

Section 2: Career & Migration Dilemmas

6. Should I move to Dubai for a tax-free salary?

Dubai offers high Nominal income and zero tax, giving you massive "global power." However, your local costs (rent/schooling) will be 3-4x higher than in India.

7. Is a $100k salary in the US better than ₹30 Lakhs in India?

Strictly by PPP, ₹30L in India often provides a higher "quality of life" (domestic help, luxury services). However, the $100k provides 3x more absolute savings for global investments.

8. Why do NRIs feel "richer" when they visit India?

Because they earn in "High PPP" currencies (USD/GBP) and spend in a "Low Cost" economy. Their $1,000 savings buys ₹83,000 worth of goods, which is 4-5x more than it buys in their home country.

9. What is the "Invisible Tax" in India?

While India is "low cost," you often pay a private tax for quality: private security, water purifiers, and elite schooling. In Switzerland or the UK, these are "public wealth" included in your taxes.

10. Can I build more wealth in Australia than in India?

In the short term, yes, due to higher absolute savings. In the long term, India’s high growth rate (7%+) means local investments (Equity/Real Estate) may outperform developed markets.

Section 3: Investment & Savings

11. Why should I invest globally if I live in India?

To protect against "Imported Inflation." If you want to buy a Tesla or a MacBook in 5 years, saving in Rupees alone may not be enough as the currency depreciates.

12. Does PPP affect my stock market returns?

Indirectly. Companies in high-PPP nations (like the US) have higher margins. However, companies in India have a larger volume of consumers. A balanced portfolio includes both.

13. Is real estate in India a good "PPP hedge"?

Yes. Local land is a finite resource in a growing economy. As India’s PPP per capita rises, land value in Tier-1 cities tends to appreciate faster than inflation.

14. What is "Lifestyle Creep" in developed nations?

It's the trap where high salaries are eaten up by high service costs (eating out, repairs). Many move abroad for wealth but end up "paycheck to paycheck" due to high overheads.

15. How does the Rupee’s value affect my global purchasing power?

If the Rupee weakens, your "Global PPP" drops. Items like fuel, iPhones, and foreign trips become more expensive, even if your salary stays the same.

Section 4: The Outlook

16. Is India’s wealth gap closing?

Nationally, yes. Individually, it's slow. India’s GDP is growing at 7%, but it will take decades of consistent growth to match the per-capita PPP of even a country like Malaysia or Turkey.

17. Why is Switzerland the "Gold Standard" of PPP?

Because it has high costs and the highest salaries. A janitor in Zurich has more "global purchasing power" than a middle-manager in many developing nations.

18. How will AI affect the PPP gap?

AI may lower service costs in developed nations (narrowing the gap) but could also threaten the "labour arbitrage" advantage that India currently enjoys in the IT sector.

19. What is the biggest risk to India's PPP growth?

Inflation in food and fuel. Since these are "basic basket" items, high inflation here directly erodes the purchasing power of the masses.

20. What is the "Rule of 3" for international offers?

A general thumb rule: To maintain an Indian lifestyle of ₹X, you usually need 3.5x to 4x that amount in a developed nation (adjusted for PPP).

21. How do I calculate my personal PPP?

Compare your "discretionary spend." If you spend 20% of your income on "wants" in India, see if you can still do that after rent and taxes in London.

22. Is "Geo-Arbitrage" the future?

Yes. Earning in USD/Euro while living in a low-cost Indian city (Remote Work) is the ultimate financial "hack" to maximize PPP.

23. What is the one thing money cannot buy in high-PPP nations?

Low cost, high-quality human labour. In India, comfort is a service. In the West, comfort is a DIY (Do-It-Yourself) project

to schedule a free introductory appointment

+91 81234 26999

FINSPIREYOU@OUTLOOK.COM

© 2026 All Rights Reserved Sukruthi Finspire You

Registration granted by SEBI (INA000020493) , Membership of Bombay Stock Exchange (BSE Enlistment number 2288), and certification from the National Institute of Securities Markets (NISM) in no way guarantee the performance of the Investment Advisor or provide any assurance of returns to Investors. Investments in the securities market are subject to market risks. Read all the related documents carefully.

ARJUN K A

pROPRIETOR sUKRUTHI